Can a 5% 30-year US Treasury bond withstand the pressure?

Since mid-May, the yield on the 30-year US Treasury bond has successfully broken through the 5% threshold, experiencing almost no resistance during its upward climb. The US market isn’t the only one facing long-end rate adjustments: since the start of the year, yields on 30-year Japanese and UK government bonds have risen by approximately 60 and 40 basis points, respectively. What are the factors behind the adjustment of long-term debt, and will it continue?

Long-term yields in developed countries are generally rising

Fiscal deficit: the underestimated long-end risk

On one hand, tariff revenues are declining after initially surging. The US’s effective tariff rate has fallen from a high of 11% to about 7%. Even if it recovers to 10% in the future, the income would only cover 60% of the Congressional Budget Office’s (CBO) expected $3 trillion deficit reduction over the next decade.

On the other hand, defense spending is rigidly increasing. With intensifying competition among great powers, technological upgrades, and the need to address shortcomings in military preparedness after the Iran conflict, US defense expenditure is facing significant upward pressure. This is not only a geopolitical cost but also a heavy fiscal burden.

Deficit pressure leading to an interest rate “death spiral”. Since the start of the year, the 5-year US Treasury yield has risen by 40 basis points, implying an additional $1.5 trillion in deficits over the next ten years. When major buyers such as global central banks and pension funds demand higher term premiums because of high inflation, US Treasury yields must continue to rise to provide enough attractiveness to absorb this new supply.

US Treasury: Tools are available, but unable to quench long-end thirst

As early as the beginning of 2025, Treasury Secretary Bessent stated that the US Treasury usually focuses more on the 10-year bond yield. At that time, the 10-year US Treasury yield was around 4.5%, which is about the current level, so the Treasury may not feel an urgent need to intervene.

If the Treasury does decide to act, the core logic would most likely focus on “reducing duration,” including expanding the scale of long-end bond buybacks through issuing more short-term bills. However, the contradiction in reality is that easily implemented measures may have limited effects; those “big moves” that could significantly turn the tide (such as sharply reducing the long-end bond supply) are extremely unrealistic under current fiscal pressures.

Federal Reserve: Higher intervention threshold under Walsh’s leadership

With Walsh taking office, the bar for adjusting monetary policy may rise significantly. Looking back to 2023, when financial conditions showed signs of tightening, the FOMC quickly adjusted its rate hike forward guidance and cooperated with the Treasury to reduce the scale of long-end bond issuance, effectively easing market sell-off pressure. However, Walsh has long advocated for shrinking the Federal Reserve’s massive balance sheet, and his policy determination means he will not easily waver based merely on short-term market fluctuations.

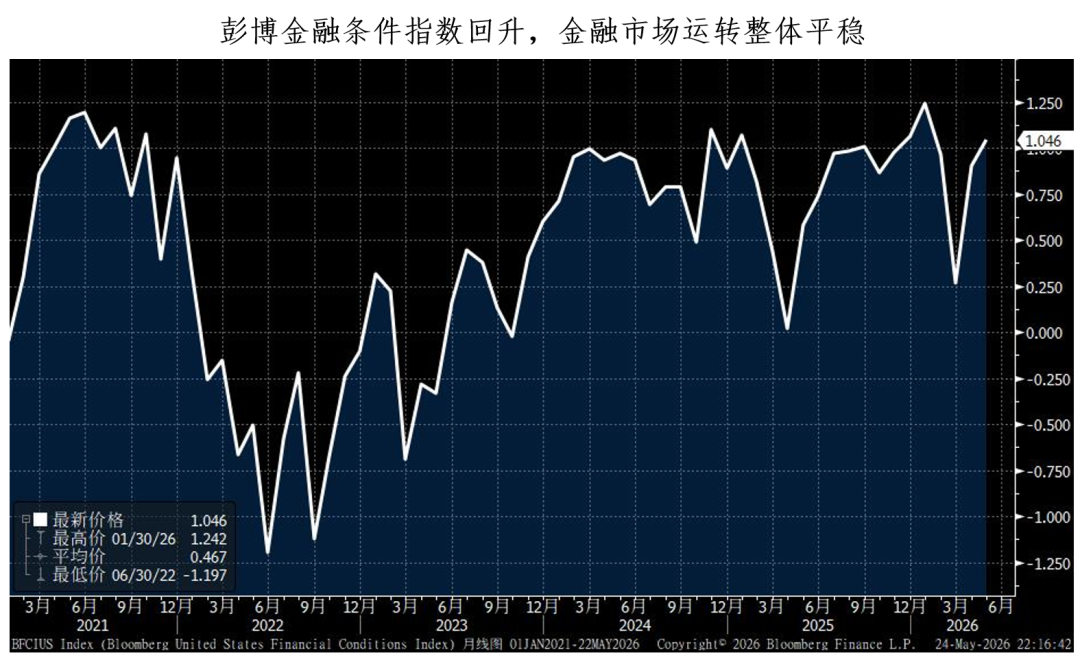

Given that the stock market remains upward, the financial markets operate smoothly as a whole, and have not seen extreme conditions where financial conditions tighten sharply or market functions break down, Walsh is very likely to “watch coldly” and allow long-term rates to remain high. For him, intervening rashly may, in the context of persistent inflation, send the wrong signal to markets and thus further escalate inflation risk.

In summary:

1,Can 5% 30-year US Treasuries hold?We believe they cannot; the 30-year US Treasury yield exceeding 5% is not the end point. Against the backdrop of resilient economic performance and worsening fiscal conditions, the term spread has further momentum to widen.

2,It’s too early to “bottom fish”: Unlike in 2023, today’s financial conditions have not materially tightened, and markets are still operating smoothly. Considering fiscal and monetary policy and institutional behavior, it may be too soon to participate in 30Y US Treasuries. For those trading interest rate retracement opportunities, 5-10Y may be a better choice.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

US strikes Iranian military targets as negotiations near completion, Rubio says

3 Altcoins Within Striking Distance of New All-Time Highs This Week

US Dollar Index holds gains above 99.00 due to renewed safe-haven demand