The US stock market is getting tense! Goldman Sachs: Remain bullish on AI but buy hedges; low-quality sectors have deviated from fundamentals

The strong surge and excessive holdings in artificial intelligence themed stocks have raised significant concerns in the market regarding the potential for a correction.

Louis Miller, Head of Equity Basket Trading at Goldman Sachs, stated in the latest research report that Goldman Sachs' trading desk remains bullish on the AI theme, but has "entered a stage relatively lacking in catalysts, making it necessary to protect the year-to-date gains." He points out that the market is now structurally divided: the fundamentals of the AI sector remain solid, so long positions should be maintained while deploying short-term downside hedges; low-quality stocks have valuations that are significantly disconnected from fundamentals, making them suitable for selective shorting opportunities.

Miller emphasized, the rally in the AI sector is well-supported by robust positive earnings revisions, and its fundamentals remain intact. In contrast, broader market gains have driven the valuations of low-quality sectors away from fundamentals, creating attractive short-selling entry points.

It is also noteworthy that Asian market momentum has clearly retreated. Coupled with the persistence of rising long-term global interest rates, elevated inflation pressures, and a fast increase in leverage levels, the bond market is signaling caution. For investors, current position management and risk-hedging strategies have become more urgent issues than directional calls.

The AI theme remains strong, but crowded positions create defensive needs

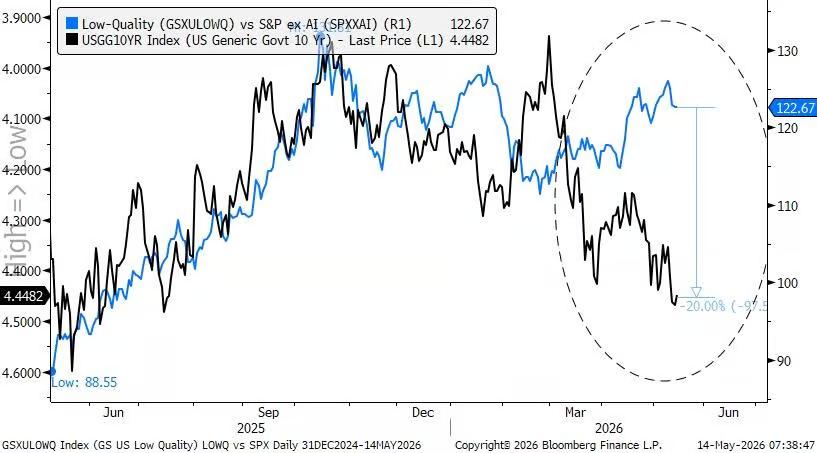

Reviewing recent markets, the performance of the AI sector has significantly outperformed other areas. Miller highlights that the Goldman Sachs US AI Data Center Basket (GSTMTDAT) has outperformed the Low Income Discretionary Basket (GSXULOWD) by nearly 100 percentage points so far this year, and posted an excess return of about 20 percentage points in the past two weeks. Top long-term growth themes have doubled in returns this year, whereas cyclical vulnerability sectors have clearly lagged.

At present, despite persistent short-term volatility, the resilience of the AI rally is still apparent. The High Beta Momentum Portfolio (GSPRHIMO) once suffered a single-day 5% drawdown, but still registered about 3% positive return for the week. However, Miller warns that historically, AI-related trades have experienced periodic corrections, and the current window is one with a lack of catalysts, providing a sound rationale for adopting short-term defensive measures.

As for hedging tools, a one-month 93% strike put option on a broad AI basket (GSTMTAIP) costs approximately 1.70% (covering 22 trading days); for loss momentum portfolios (GSXULMOM), a bullish spread protection collar strategy costs around 0.7%. Both are cost-effective measures for managing downside risks in the current climate.

Energy security emerges as the most favored theme beyond AI

Among non-AI themes, Miller points out that energy security is now considered by Goldman Sachs as the most compelling global investment focus.

In US markets, the Domestic Solar Basket (GSXUSOLR) has stood out from the broader Power theme (GSX1POW1), showing an independent upward trend. Miller believes that as the midterm elections approach, the market's heightened attention to power supply and electricity prices will persist, and the earnings outlook for GSXUSOLR supports further upside potential for this rally.

Across the Atlantic, the European market also holds opportunities within the power theme, but for entirely different reasons. Global capital interest in the region has once again faded, but this "low crowding" actually creates structural opportunities. Goldman Sachs has doubled down on European power themes (GSXEPOWR)—the breadth of earnings revisions in this basket is currently at its historical peak and is unaffected by the US midterm elections.

Consumer sector: crowded shorts, short-term results unlikely to alter macro caution

In the consumer sector, Miller says it is not advisable to continue increasing shorts. Various subsectors, including Low Income Discretionary (GSXULOWD) and Mid Income Discretionary (GSXUMIDC), have underperformed the S&P 500 by a cumulative 10 to 15 percentage points since the beginning of the year. Given how crowded short positions already are, adding further shorts faces the risk of short squeezes in the near term.

Goldman Sachs consumer industry expert Scott Feiler notes that some consumer goods companies (including ONON, BIRK, ARMK, YETI, etc.) have already posted decent results this week, and most representative stocks are expected to beat expectations with little guidance pressure.

However, Miller cautions from a macro perspective that one should not become overly optimistic due to short-term performance improvements. "Stagflation pressure eroding consumers' wallets remains the core basis for fundamental judgments," he says. "One should remain calm about any sharp gains."

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

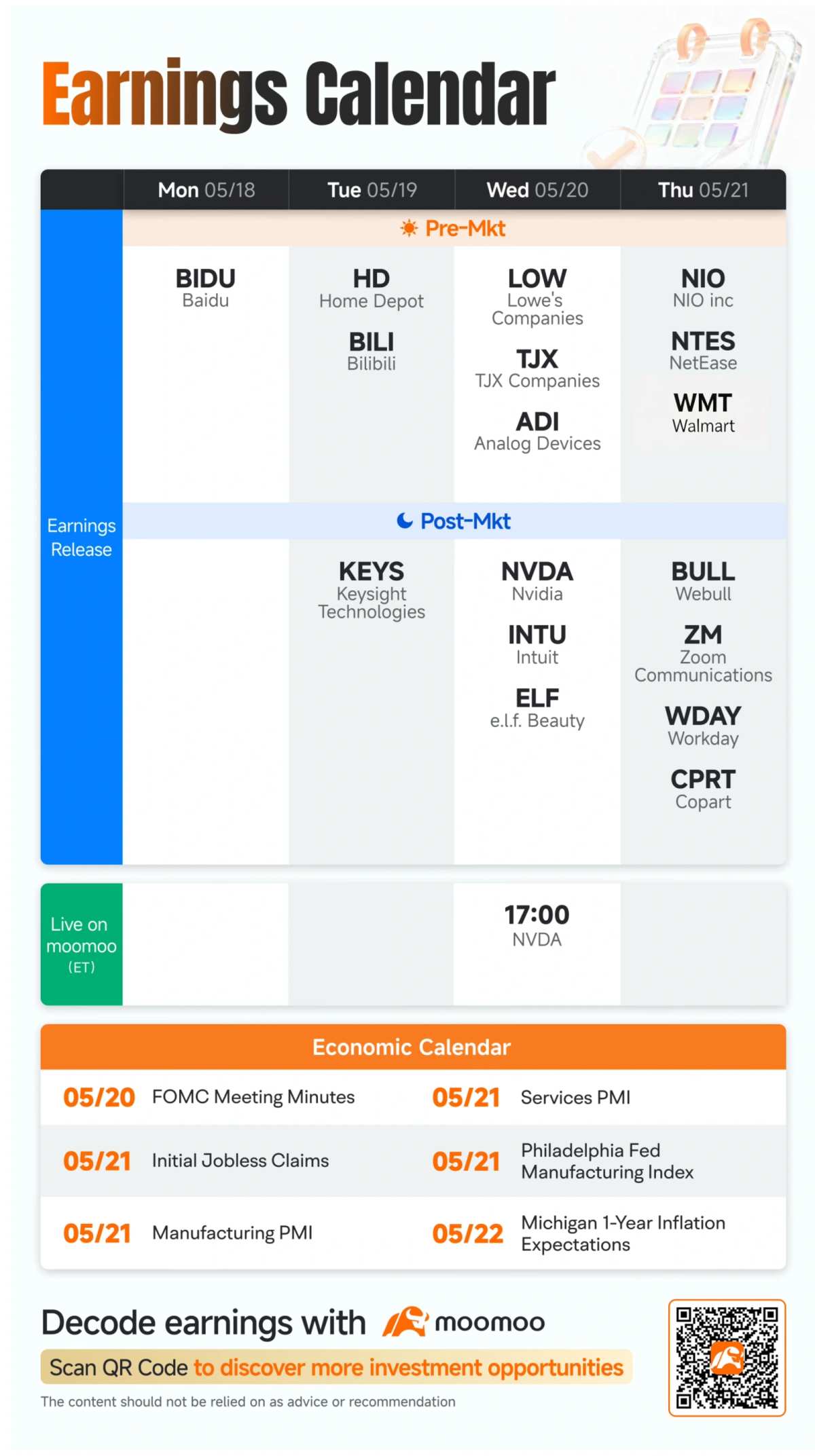

What to Expect in the Week Ahead (NVDA, WMT, HD Earnings; Fed Meeting and CPI Report)

ESIM fluctuated 99.8% in 24 hours: Severe price volatility driven by low liquidity